Predicting a Post-Election Polymarket

An analysis of Polymarket and the challenges that lay ahead

In my last piece, I delved into the world of memecoins, highlighting how they can serve as vehicles for delivering ideas, with narratives intertwined in financial speculation and cultural commentary. Now, let's turn our attention to prediction markets, which are striving to achieve a similar goal but through a distinctly different approach.

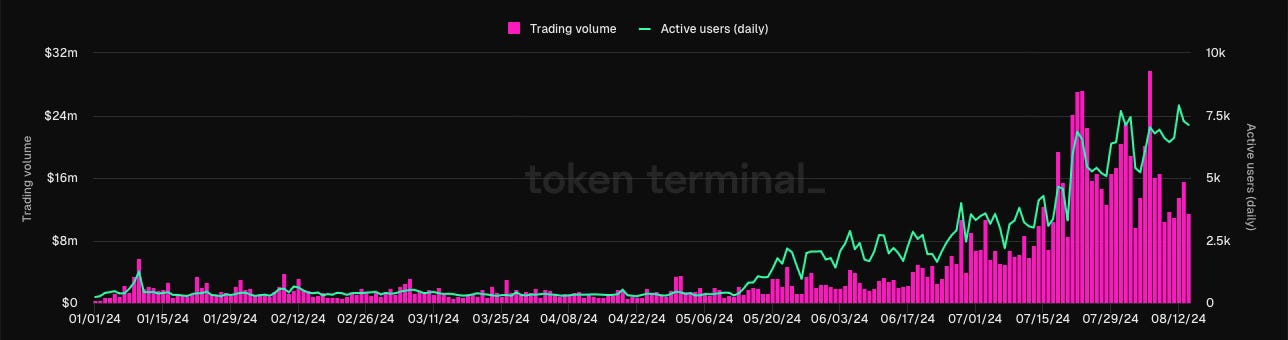

Over the past six months, Polymarket has emerged as one of, if not, the most successful consumer crypto application to exist thus far. A new asset class has formed, blending speculative elements of crypto markets with wisdom of the crowd to predict the future of events. With backers like Peter Thiel, the onboarding of political experts like Nate Silver, and integrations across platforms such as Substack and Perplexity AI, the future looks promising for Polymarket, attracting mainstream attention at levels no individual crypto application has seen before.

The platform allows people to bet on current happenings across sectors, creating a new spectrum of truth in an era where trust in traditional media sources is waning. On top of that, it’s a cleaner, more risk-adverse alternative to aping into 1 of a 100 different memecoins all focused around one topic as an attempt to make money off cultural relevance. In general, the game is also more “fair.”

At its core, Polymarket is a game of prediction. The platform’s users engage in betting, not just for profit, but as a method to refine and sharpen collective foresight. This dynamic has made Polymarket especially powerful in the political arena, where it has accurately forecasted key events, such as Joe Biden dropping out and JD Vance's selection as Vice President. The platform’s ability to facilitate collective insights into actionable predictions has positioned it as a reliable alternative to traditional news sources.

However, many still question the long-term retention of the platform. Although politics has been a great draw for Polymarket, do users care about the other markets outside of Presidential elections? What happens once the election ends? To get closer to answering these questions, we have to dive into some data.

Diving into the Data

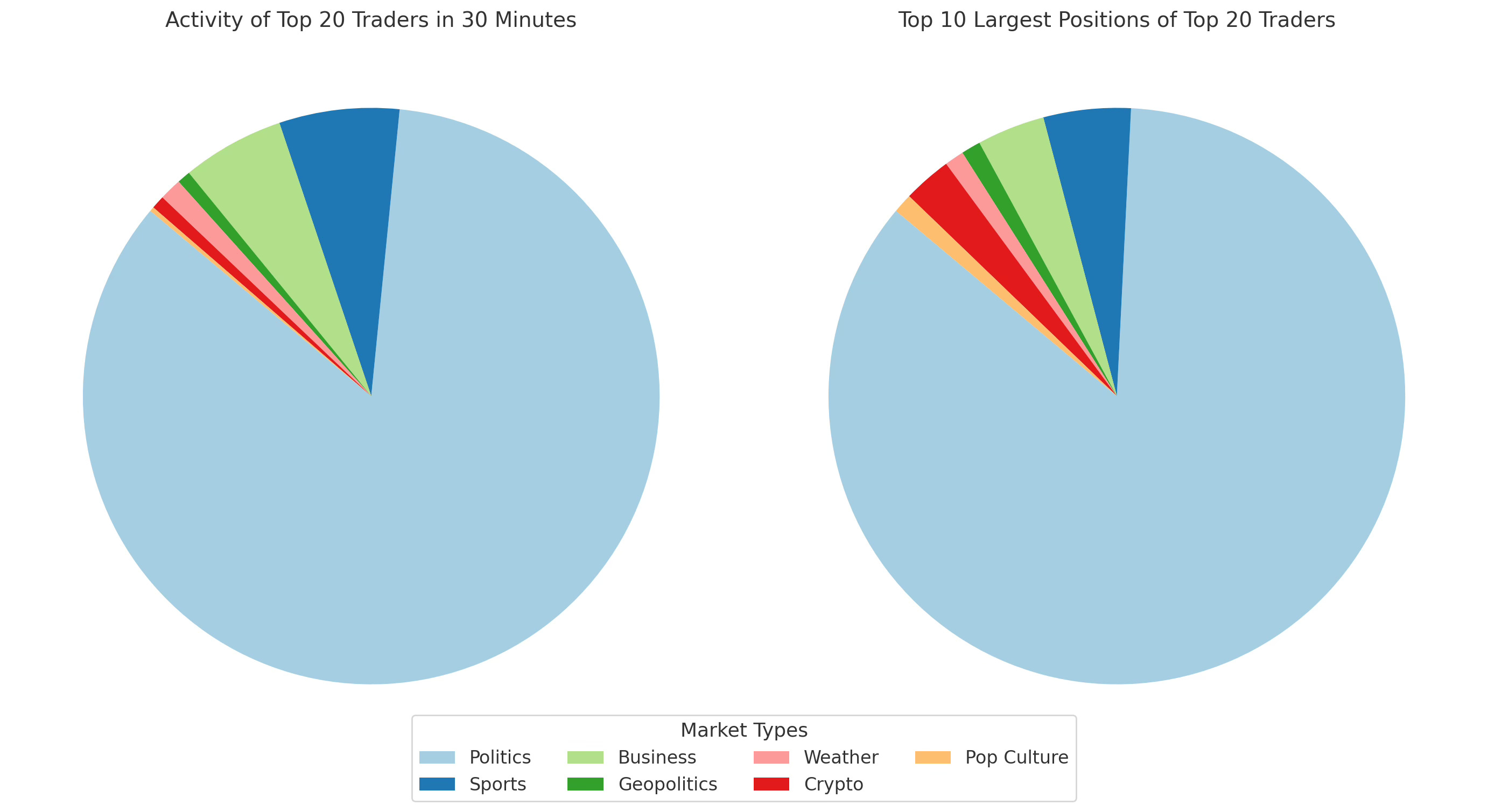

Snapshotting their last 20 trades, the top 20 monthly traders on Polymarket made, on average, 16.95 politics trades compared to 0.52 trades in other markets. This stark contrast indicates a significant preference for politics-related trades among the top traders. Non-political trades are spread across various categories, suggesting a diversity in market interests, yet each category sees significantly fewer trades on average compared to politics.

Interestingly, some traders have a higher concentration of trades in non-political markets. For example, 'qrpenc' has 7 business trades and 6 sports trades, and 'bama124' has 14 business trades and 5 weather trades. This indicates that while the overall average is low, specific traders show significant activity in these markets. While the top 20 traders predominantly engage in political trades, there is notable but limited engagement in other markets, with significant variability among traders.

Sports, business, and crypto positions exhibit higher standard deviations relative to their means, indicating significant variability in how different traders engage with these markets. Some traders may hold several positions, while others may not participate at all, or they may be participating, but with smaller size due to low liquidity in those markets.

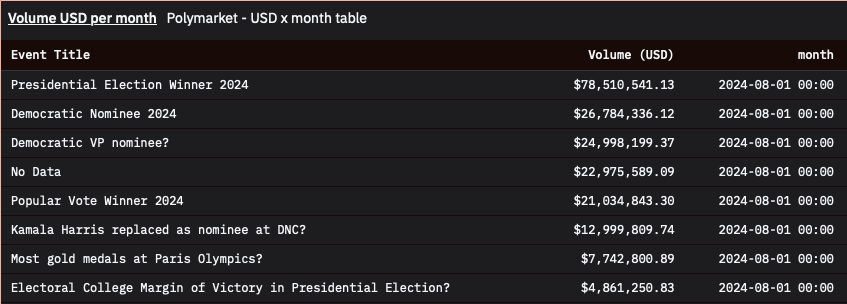

The political markets by far have the highest volume and liquidity on the platform. High liquidity markets attract larger levels of attention and mindshare, allowing the market to quickly and accurately adapt to events relevant to moving those specific markets. For example, in the presidential odds, Kamala Harris has made drastic moves upwards in the past few weeks, at one point even surpassing Donald Trump. This can be correlated with recent events surrounding both candidates that gave her advantages.

These high-volume, high-liquidity markets correlate well with present public sentiment. In contrast, smaller markets on the platform aren't as actively traded, and therefore, they don’t correlate as effectively with public sentiment. This disparity highlights the importance of liquidity and volume in ensuring that prediction markets remain reflective of broader trends and sentiments.

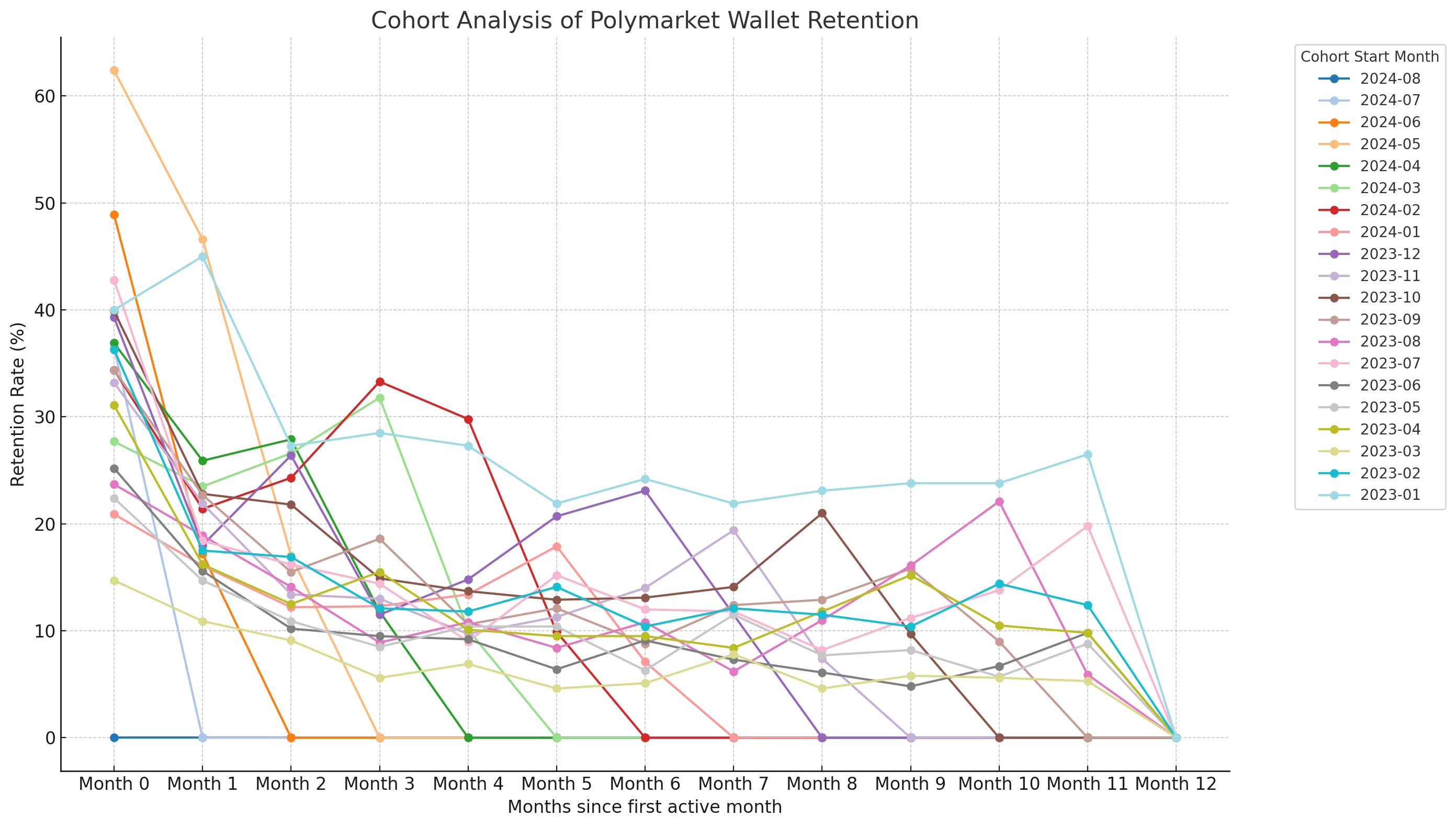

Meanwhile, the wallet retention data for Polymarket provides a revealing look into the engagement and retention patterns of users over time. Each row in the data represents a cohort of new users (wallets) who joined Polymarket in a specific month, with subsequent columns showing the percentage of these users who remained active over the following months.

From the recent cohorts in 2024, we observe significant initial engagement with a notable number of new users joining each month. For instance, in June 2024, 19,676 new wallets joined Polymarket, but only 48.9% of these wallets remained active in the following month (July 2024), and this percentage further dropped to 17.2% by August 2024. Similarly, the July 2024 cohort started with 26,406 new users, but only 36.5% remained active into August 2024.

Long-term retention trends show a consistent pattern across all cohorts, with a substantial decline in active users after the first month. For example, the May 2024 cohort saw 11,342 new wallets, with retention falling from 62.4% in June 2024 to 46.6% in July 2024, and further down to 17.0% by August 2024. This trend is echoed in earlier cohorts from 2023, where retention rates continue to decrease steadily over time, with only a small fraction of users remaining active after several months.

Navigating Challenges

Can prediction markets effectively measure an idea's value? I believe the answer is yes, to a certain extent. Just as memecoins come with certain challenges, prediction markets come with others complicating their effectiveness in delivering the value of an idea, but these challenges significantly differ due to market design approaches.

Challenge #1: the dilemma of hyper-relevance

The dilemma of hyper-relevance poses a significant challenge for prediction markets. How do you determine what counts as hyper-relevant and what markets users actually want to bet on? Kyle Samani at Multicoin Capital recently explored the concept of regularity within prediction markets. To justify spending on customer acquisition cost (CAC), platforms need a large lifetime value (LTV) of users, which in turn requires high volumes of activity across the platform. However, most of this volume is currently concentrated in political markets.

Samani argues that the lack of regularity within the platform results in a lack of recurring bets, which creates no substantial LTV and, consequently, doesn't justify spending on CAC. This regularity is crucial for maintaining user engagement and driving sustained volume on the platform.

Regularity and hyper-relevance are intertwined. In fact, you could say regularity is relevance. What we deem to be regular is also what we find the most relevant in our day-to-day lives. Prediction markets face the challenge of needing regular, underserved, yet also hyper-relevant markets. Solving this issue involves navigating a complex web to find the perfect blend of topics that people not only find engaging but are also engaging enough to bet on. The absence of regular markets leads to sporadic engagement, making it difficult for platforms to build a loyal user base and achieve the necessary volume for long-term success.

Challenge # 2: the complexity of user profiles

So if you have sporadic engagement, and you can’t identify who your loyal user base is, it leads you to further difficulties in identifying the platforms user profiles. When considering CAC for prediction markets, it's essential to understand which customers are being targeted. This complexity makes it challenging to justify spending on CAC because the typical customer profile for prediction markets is not particularly clear. So who are these users participating on the platform right now, who will continue participating in the future, and why will they continue participating?

A recent piece by Nick Whitaker and J. Zachary Mazlish titled "Why prediction markets aren't popular" delves into this issue. While I don't agree with the article's overall premise — given the visible popularity of platforms like Polymarket — the authors make several key distinctions regarding user profiles that are hard to ignore.

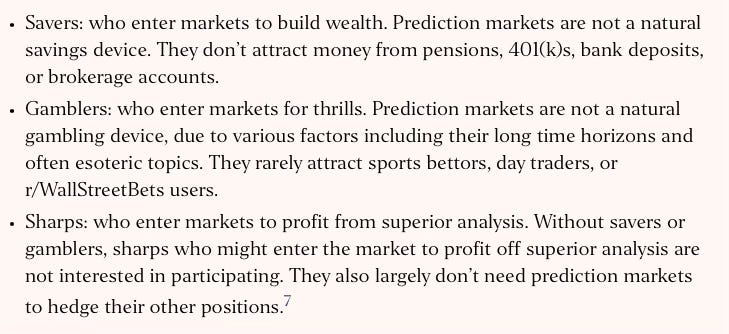

Understanding these distinctions is crucial because it is not entirely clear who should be the priority in prediction markets. Savers are unlikely to use prediction markets because they are zero-sum/negative-sum games, where one person's gain is another's loss. This zero-sum nature is contradictory to the 5% annual gains a saver is chasing.

Gamblers, on the other hand, seek quick resolutions and immediate gratification. The thrill of sports betting and traditional gambling often comes from the fast pace and immediate outcomes, something that most prediction markets, with their longer time horizons, fail to provide. This ties back to the concepts of regularity and hyper-relevance—there isn't much on Polymarket that offers the immediate excitement and quick turnaround that gamblers crave.

This leaves the final category: the sharps. These individuals participate based on their belief in their superior intellect and analysis. However, the piece argues that without savers to provide the necessary capital and profit potential, the market dynamics don’t work. Additionally, sharps prefer to trade against gamblers, but since gamblers aren't drawn to prediction markets, sharps end up competing against each other, reducing liquidity and market viability.

The complexities of user profiles create a challenging landscape for prediction markets. Who remains as the regular user on Polymarket, and does that user provide sufficient LTV for the platform?

Challenge #3: the struggle of user retention

Now going back to the data we saw helps us highlights the third challenge faced by Polymarket: maintaining user engagement beyond the initial period. Despite the high influx of new users each month, the platform experiences a significant drop-off in active wallets within a few months. This rapid decline in user activity underscores the difficulty in sustaining long-term engagement on the platform. High initial engagement may be driven by curiosity or the allure of specific high-stakes political markets, but the challenge remains in keeping these users engaged with other market categories once the initial interest wanes.

While we can't definitively categorize these profiles, we can draw assumptions about the users who are returning and those who are leaving. Each cohort likely comprises of a mix of sharps and gamblers. The users who remain active are probably the sharps, feasting on the gamblers by making strategic, educated trades. These sharps might even be using AI agents to enhance their trading strategies—more on that later. Meanwhile, the gamblers are those betting on crazy returns without necessarily having full knowledge of the markets they're engaging in. These gamblers are likely contributing to some of the random low-volume, low-liquidity markets that sharps tend to avoid. The gamblers arrive in waves, bringing more sharps into the new cohorts, but only the sharps end up staying. This dynamic creates a cyclical pattern where new users are attracted by the excitement of potential gains, but only those with a deeper understanding and more strategic approach continue to engage over the long term. Over time, gamblers begin to arrive in smaller numbers due to low returns, lack of interest/excitement, and lack of skill in meaningful trades. All that’s left are sharps and then we run into the problem of sharps not wanting to play against each other but rather savers or gamblers, as they feel they can win in the market against them.

The retention issue ties back to the earlier challenges on the complexity of user profiles and the dilemma of hyper-relevance. Without a clear strategy to provide regular, diverse, and engaging markets that cater to various user profiles, Polymarket struggles to maintain its user base. The focus on high-liquidity political markets, while initially attractive, may not be sufficient to sustain long-term user engagement across the platform.

Emergence of AI Agents

When it comes to the sharps, it’s hard to say whether it's actually these guys trading or not. Many of them might have fixed strategies to only fill orders and seek rewards from Polymarket as market makers, but they also might be using AI agents. Companies like RoboNet and Olas Network are offering new primitives to take prediction market participation to the next level using AI. Sharps using AI agents can leverage advanced algorithms to predict market movements more accurately, outmaneuvering gamblers who rely on less sophisticated methods. The advantage not only helps the sharps remain on top of the markets but also discourages the gamblers who quickly realize their losses.

Amongst the top 20 traders, you’ll see occasional times where there will be no movement from them but within an extremely short period of time, you’ll suddenly see a large number of trades being made with very specific and strategic amounts correlated to their positions, signifying potential use of these AI agents. We can’t know for sure whether these sharps are relying fully on the AI agents or just on small transactions but the usage is pretty apparent, creating higher levels of competition with the most elite of the traders on the platform.

Conclusion

Data can tell many stories, and how we perceive that data is often shaped by our preconceived notions. Yes, the numbers highlight retention issues and show a heavy focus on politics. But despite these apparent challenges, I believe there’s a future here for prediction markets. The journey to gaining widespread traction in prediction markets takes time, and I view this election cycle as more of a test run for Polymarket than anything else.

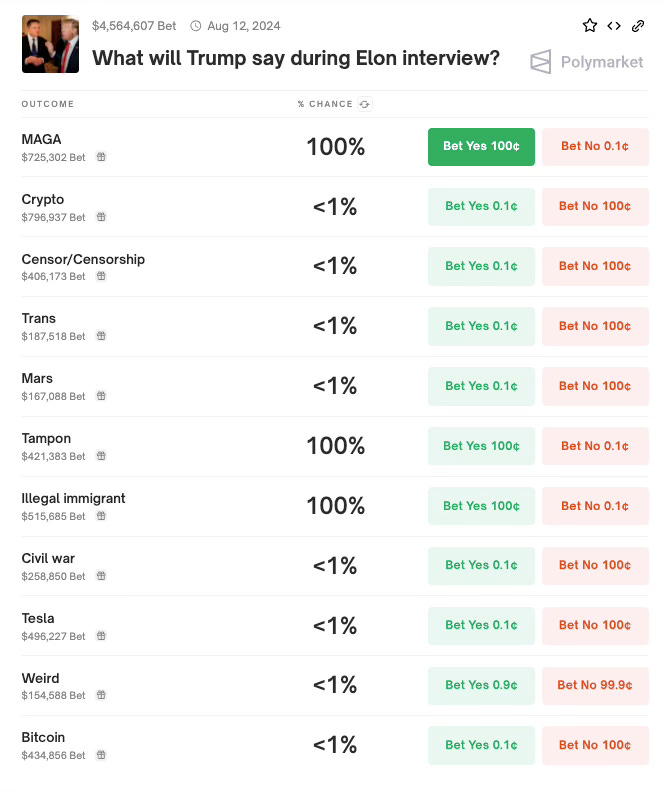

Elements of regularity have begun to emerge within the platform. Highlighted events like Kamala’s speech and what Trump was going to say during his interview with Elon Musk integrate people’s attention into the application on a live basis, similar to the psychological functions of mainstream sports betting.

We’ve only just begun to see what prediction markets can achieve, with more features and capabilities still on the horizon. While it’s likely that volume may dip post-election, it's essential to recognize that we are dealing with a new kind of market—one where social participation is deeply intertwined with financial mechanisms. Politics might remain the central element, but that doesn’t mean other ideas can’t find their place within these platforms. Even after the election, the aftermath could spark new markets: Will there be a peaceful transfer of power? Will the election results be contested in courts? Will civil unrest follow? Will there be WW3?

In this context, underestimating the potential of prediction markets, even during quieter times, could be a mistake. I believe that I, amongst many, have asked the wrong questions about Polymarket. It’s not about delivery of ideas, it’s not about reliability, it’s not even a comparison with memecoins either. It’s about understanding the broader role they play in our social constructs. The evolution of these platforms is just beginning, and their true impact may only become clearer with time.